Most of you reading this likely contribute to your employer's 401(k) plan. And a good percentage of you also receive matching contributions from your employer. Or if you own your own business, you might contribute to and also be responsible for the matching contributions. I imagine you've heard these employer matching contributions referred to as "free money". Sure, we can call it that and if it feels good, do it. If you aren't taking advantage of your company's match you're leaving money on the table. I guess that's where the idea of "free money" came from. I'm not sure. At the end of the day, the reality is you're not getting paid your full compensation.

Wait, what did he just say?!

Yeah, you heard me.

In today's retirement landscape, the employee is (mostly) responsible for funding their own retirement. Pensions have and are going the way of the dinosaur. Today, the 401(k) is the primary retirement investment vehicle. The average percentage of eligible employees who have a balance in their 401(k)plan is 88.7 percent, and 84.9 percent made contributions to their plan in 2016*.

From the employer's perspective, matching contributions have a couple of key benefits:

Since they're paid to the employee, matching contributions to a 401(k) are viewed as compensation. In turn, they lower an employer’s taxable income for the year, also reducing their tax liability.

When it comes to hiring new employees, the 401(k) match can definitely help employers stand out against the competition.

These two points are important to keep in mind. So let's talk about what the 401(k) Match is and why those two points above should really matter to you. Like really matter.

The 401(k) Match

A 401(k) match happens when an employer agrees to "match" an employee's contribution. This typically ranges from 3% - 6% of an employee's compensation, or salary. On top of that, the employer can match 100%, or dollar-for dollar, all the way down to 25%, which would be $0.25 of the employer's money for every dollar of your money. On top of that, they can put a cap on how much they'll contribute. And sometimes the employer puts a cap on how much of your salary they'll match to. Confused? Let's break it down…

Example #1

Johnny recently started working for The ACME Company. They pay him $100,000 per year. ACME has a generous match. They match 100% (dollar for dollar) up to 6% of his salary.

$100,000 x 6% = $6000.

Cool? Cool.

Knowing this then we know Johnny, at the bare minimum, should be contributing $6000 to his 401(k) to take full advantage of The ACME Co matching program. If he does this, then he'll contribute $6000 and The ACME Co will also contribute $6000. As we'll see in a little bit, this is a big deal.

Example #2

Johnny's sister, Jenny, works for ACME's main competitor - The Roadrunner Inc. Jenny earns $200,000 per year. The Roadrunner Inc also has a generous match. They match 75% (or $0.75 per $1) up to 5% of Jenny's salary.

The math here gets a little tricky. First, we have to calculate 5% of Jenny's salary. So $200,000 x 5% = $10,000. Now we take $10,000 and multiply that by .75 (75%).

$10,000 x 75% = $7,500.

Boom! For Jenny to take full advantage of her company's matching contributions she has to contribute $7500. And by doing just that, she's able to double her contribution.

Okay, now we know what the match is and we've seen some examples of how it works. Let's address our two points above.

But It's Free Money

This is a pretty common statement around the matching contributions. I'm gonna have to disagree though. In point number one above, we know that 401(k) matching contributions are viewed as "compensation". The reality is our friend Johnny's full compensation is $106,000 and Jenny's full compensation is $207,500. The company you work for has budgeted and allocated these dollars to you. You simply don't receive the money directly in your paycheck.

I can't imagine a single one of you reading this would voluntarily take less money in your paycheck. By not taking advantage of your company match this is, in essence, exactly what you are doing.

It's a shift in mindset or how we frame it. But remember, it's still considered "compensation".

Know What Your Match Is

For those of you considering a move to another/new company, listen up. Take a few minutes to calculate the real dollar amount of your match. Remember, that's money earmarked for you. That way when you consider compensation offers from your new prospective employer, you can tell them what your true compensation is. And at the very least you'll know if their match is worse, the same, or better than your current employer.

Your Future Self Will Thank You

Other than not receiving the full compensation you're entitled to, missing out on the matching contribution can impact your retirement. Let's bring our friend Johnny back into the picture. We know he earns $100,000 and if he contributes 6% of his pay to his 401(k) he also earns his additional 6% of compensation via the match.

What if he only contributes 3%? Well, we know at least one fact: he's leaving 3% or $3000 of compensation out there. On top of that, the 3% is losing out on the opportunity to grow and compound. This is important.

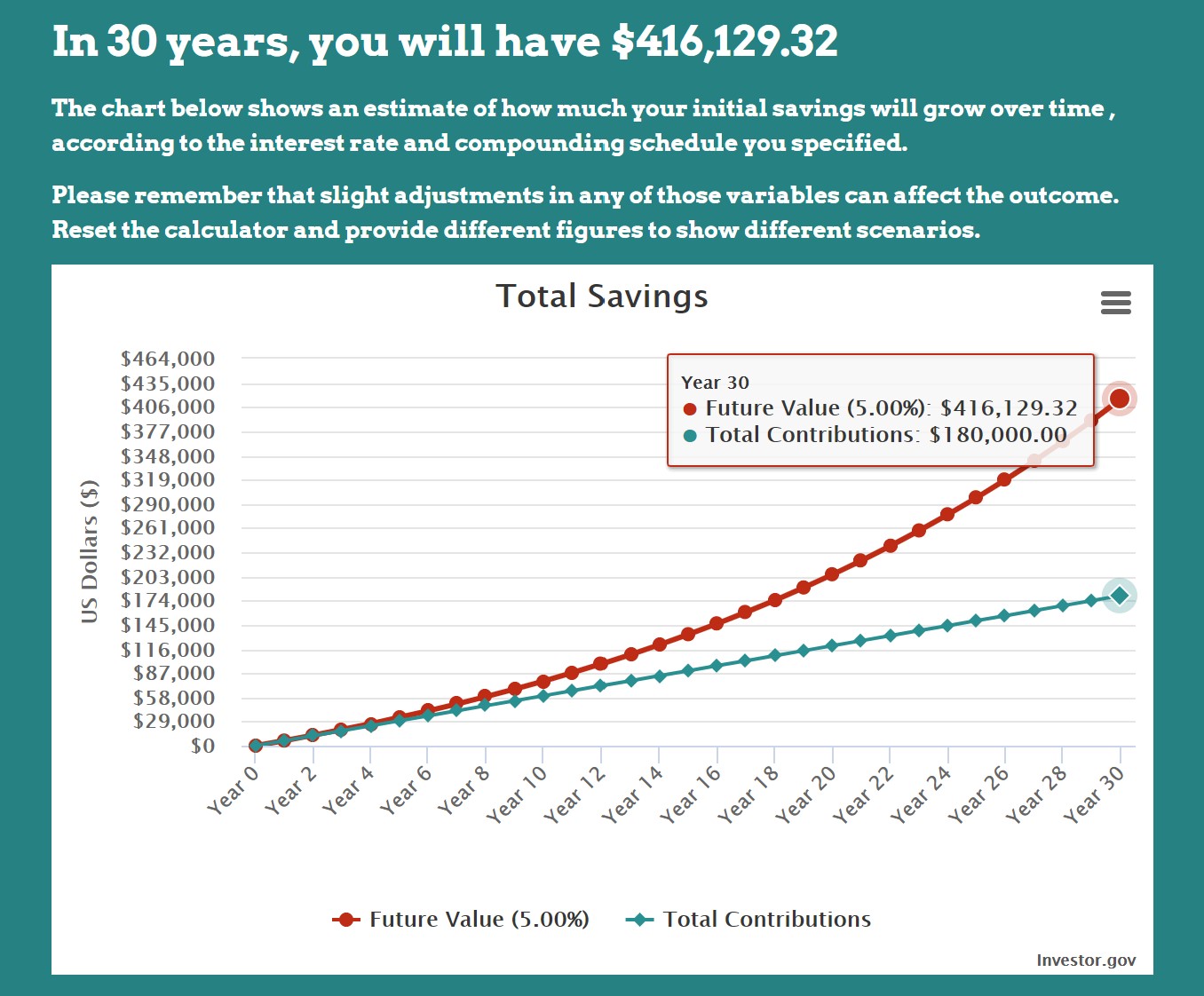

Johnny gets paid 2x month and he puts $125/pay period or $250/month (times 12 = $3000) into the ACME 401(k) plan. Let's also assume ACME matches in conjunction with the employee contribution. So again, ACME match is $250 x 12 = $3,000. That's a combined total of $6000 per year going into Johnny's 401(k).

As we can see above and to the right, Johnny's investment earns a very stable and consistent 5% for the next 30 years and results in a hypothetical account balance of ~$416k.

Johnny is smart. In fact, he's probably saving more but to keep things simple our next example shows him saving just the right amount to receive his full compensation. Now he's saving 6% of his $100k salary and that's $6000/year or $500 per month. And ACME is matching his $1 for $1 so that's also $500/month. For simplicity sake, Johnny's total 401(k) contribution = $1000/month. All variables are the same as above but before we get to it I bet this hypothetical account balance will be exactly double what it was above…

Shocker, right? LOL. Of course it should be double.

The ROR was the same, the time frame was the same. We simply doubled our contribution amount. In a linear formula, well, you can figure that out. Now Johnny has ~$832k simply because he saved 2x and received 2x more of his matching "compensation".

That’s a win-win and his future self will most definitely thank him for it. He a) saved more money and b) earned his full compensation by doing so.

Still not convinced? Here's how important the matching compensation is. When Johnny contributed $6000 instead of $3000, he "earned" $3k per year more in compensation via the match. That's $90k over 30 years. Not a ton of money over 30 years.

But because he also invested it he was able to turn that $90k into nearly ~$208,000. Put differently, he was able to turn 3% of his compensation into 25% of his hypothetical account value.

Wait, what?!

$208,000 divided by $832,000…yup, that's 25%. And that’s a lot more than 3%.

Psst - remember, math ≠ money.

Wrapping things up, let’s have a quick review of what we talked about today:

Remember, it’s not free money. It’s compensation and it belongs to you.

Whether you’re looking at your current employer’s 401(k) plan or evaluating a future employer, be sure to know the value of your matching compensation.

Take advantage of the matching compensation and compounding interest. Both are your friend!

Have questions or not sure where to start? Let me know or book a quick call with me.

*Plan Sponsor Council of America (PSCA), 60th Annual Survey Reflecting 2016 Plan-Year Experience, February 12, 2018