We've all been in this situation before: "Should I do X or Y?" Financially, we are constantly faced with these dilemmas.

Should I save for retirement or my kid's college education?

Should I invest in the 401(k) or the Roth 401(k)?

Should I invest a lump sum or systematically?

This time I want to tackle an age old debate:

Should I pay off my mortgage early, or should I use the extra money and invest?

First, I think it's a strategy many of us have heard our parents and/or grandparents talk about. Some of us may have some biases to contend with when it comes to making personal financial decisions. And I want to get into some of the history of interest rates so you have context.

For most of you reading this, all you know is low interest rates. Since 2000, the average 30-year fixed mortgage interest rate is 5.25%. That's ridiculously low. You have no experience with the pain of the 1980's when 30 year fixed interest rates were north of 15% (yes, 15%!!!!) for most of 1981 and 1982, and above 10% for the majority of the 1980's. Imagine locking in a smooth 18.45% in October of 1981. Hard pass.

So if we look back, we can compare the 30 year mortgage interest rate against what the stock market did over the same time frame. For our example, we'll use the S&P 500 Index as our "market." Our first study period covers 1964 -1988 and our second study period covers the last 30 years. Here's what I found:

Look at that average 30-year interest rate…9.79%. Egad!!

If our mortgage rate was in the 7%, 8% or higher range, yeah, why wouldn't you want to pay that sucker off ASAP? We'd all be drowning in interest payments if we had those rates today.

Compare that with our most recent study period and we see the S&P 500 Index returned far better than what our 30 year mortgage was costing us, on average.

My comparison is not to put the stock market vs interest rates as apples-to-apples. I simply want to provide some context & history around how the two eras varied. And I think we can start to see how some of our biases and "financial lessons" could be formed. We are often a byproduct of our surroundings. And I think "pay your mortgage off early" is one of those. Not that there's anything wrong with it. But let's see.

Here are our parameters:

30-year Mortgage

4.5% interest rate

$500,000 loan amount

Monthly payment = $2533.43

If we pay the mortgage as scheduled, it takes us exactly 30 years and we pay $412,033 in mortgage interest. Pretty standard, no surprises.

Some may gag at the amount of interest we paid. And if so, then you probably want to get this puppy paid off so let’s do that.

You decide you're going to pay an extra $1000 per month toward the mortgage. Now the payment = $3533.43.

An extra $1000/month means it takes us 203 months, or just under 17 years to pay our house off. Pretty cool, huh? And we've paid $214,050 in mortgage interest over that same time frame. That's nearly a $200,000 savings in mortgage interest. Rad!

But what if we kept the $1000 per month and instead of sending it to the mortgage company, we saved and invested it?

We've seen the data above and know that over longer periods of time, the S&P 500 produces pretty favorable returns. We have a 30 year time horizon, just the same as our mortgage. And for giggles, we'll earn a constant 6% rate of return. And since we're using a constant rate of return with no down markets, 6% seems reasonable.

Drum roll…

At the end of the 30 years, we'd have our mortgage paid off and an additional $1,004,515 in an investment account. Not too shabby. And some of you might already be jumping up to grab the $1m and run.

Not so fast.

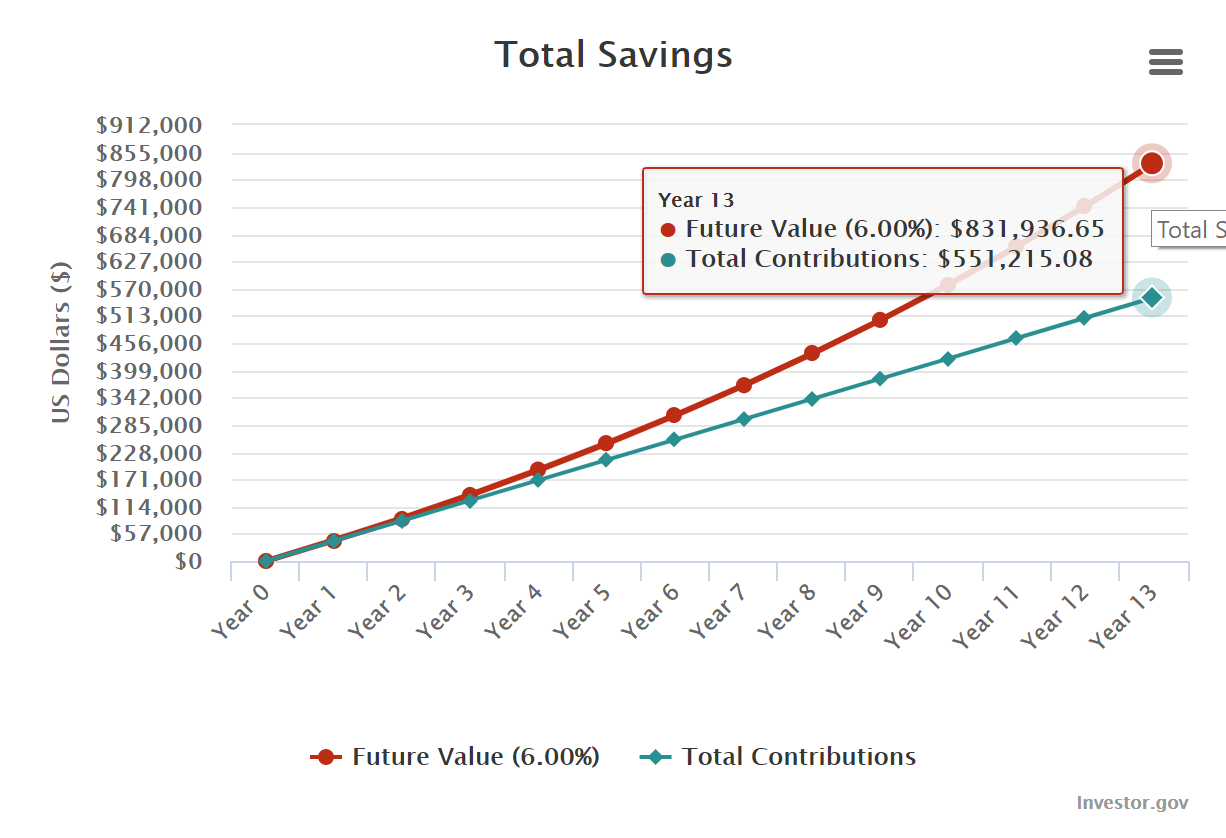

When we paid the mortgage off early we did it 17 years. That means we still have 13 years to play catch up with our scenario where paid the mortgage down as scheduled. What that means is we can take our mortgage payment $2533.43 PLUS our $1000 = $3533.43 and now we get to invest it.

Remember: we're investing more than 3X the same amount. We'll get the same constant 6% rate of return, because all things are equal in this comparison. And 13 years later, we have $831,936 which we'll round up to $832k.

Quick recap:

We pay the mortgage off early + we invest for 13 years = $832,000

We pay the mortgage as planned + we invest for 30 years = $1,004,000

Some of you are all set to take the money and run. And I don't blame you.

And some of you might be saying, "Hey, what about the mortgage interest? Because we paid our house off early, don't we realize a mortgage interest savings?"

Yes, but it's a savings you don't really feel. Why? Because cash flows in both examples are the roughly the same. Here's what I mean by that.

normal payment schedule

If we pay off the house over 30 years, as scheduled, we pay $500,000 toward principal and $412,033 toward interest. Total to be repaid = $912,033. And we're putting $1000 per month away and investing it. So that's another $12k per year x 30 years = $360,000.

Total cash flow = $1,272,033

accelerated payment schedule

If we pay off the house early, we pay $500,000 toward principal and $214,050 toward interest. Total to be repaid here = $714,050. Now over the next 13 years, we're putting $3533.43 into an investment account (that's our mortgage payment $2533.43 PLUS $1000 extra). That's $551,215.

Total cash flow: $714,050 + $551,215 = $1,265,265

Over 30 years our cash flows, or the money we used to pay off our house and invest, are basically the same in both strategies. Yes, by paying off the house early you technically do save money by not paying as much mortgage interest. But we lose something I'd argue is more important: time value of money.

We can also call this compounding interest.

By paying our mortgage off early and then investing, we lose the opportunity to compound our money over a much longer period of time (30 years vs. 13 years). AND it requires $3500 per month to get to $832,000 vs. $1000/month to get to $1,000,000.

Never mind the fact we have a much shorter period of time to invest, which means we have to get extremely lucky in how we experience rates of return. Our $1000/month strategy has an increased chance of success because we have a longer time horizon. This should allow us to better smooth out the ups and downs typically associated with investing. And investing should be a long term endeavor.

All of this is great, right?

Maybe in a perfect world. Where rates of return are perfectly linear (no chance). And where our entire future financial lives go exactly according to plan (rarely happens). In a perfect world, this comparison makes perfect sense. But I've yet to meet someone whose entire life has gone exactly according to plan over 5 years, let alone 30.

So which strategy is right for you? If you've been following along, you probably know the answer…it depends. Because it's personal.

Here are some factors to consider in your decision:

what are your attitudes toward debt?

what are your attitudes toward risk?

are you a disciplined and diligent saver?

are you a disciplined investor?

do you favor liquidity?

Other factors such as tax brackets, tax drag of investments, and even tax deductibility of mortgage insurance could also be considered in your decision.

I talk a lot about where your money goes, and why. Answering the questions above can help you decide which strategy makes the most sense for you. In addition, working with a Certified Financial Planner™ can help you better define where your money goes, and why.

Not sure which is the right strategy for you? Let’s find out…